Who We Are

Global Quantitative Advisors (GQA) is a quantitative finance and technology firm specializing in delivering cutting-edge solutions to a global clientele, spanning financial and industrial enterprises. Our team is composed of highly skilled professionals with diverse educational backgrounds in mathematics, computer science, statistics, physics, and engineering, coupled with extensive experience.

More about us

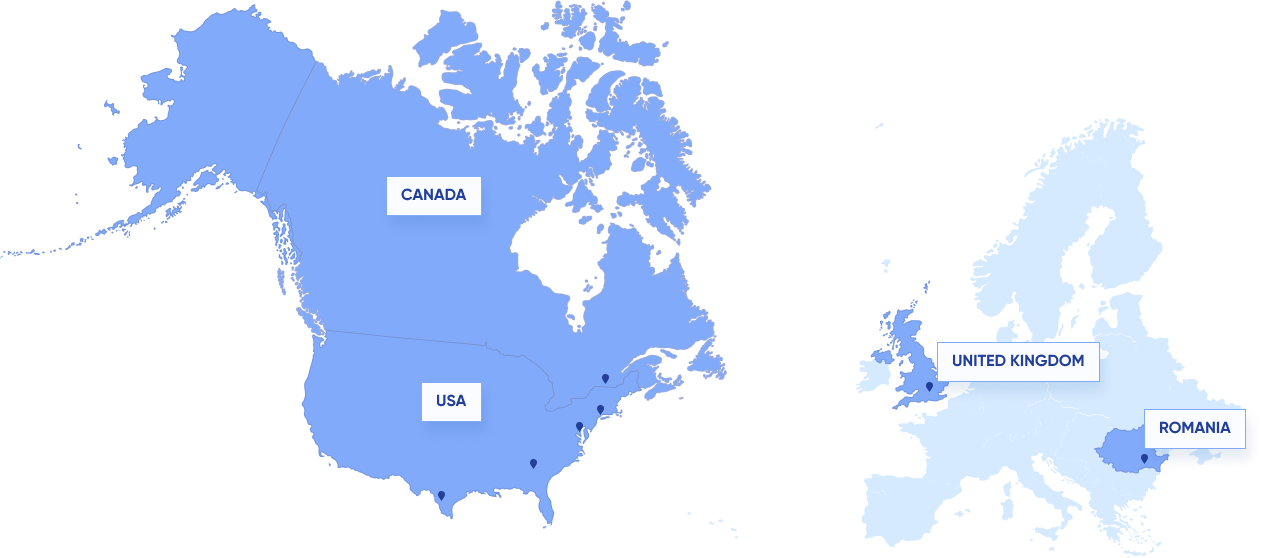

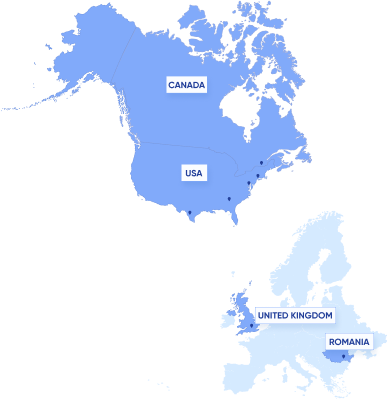

Where Our

Experts Are From

-

NEW YORK

-

BOSTON

-

HOUSTON

-

MONTREAL

-

LONDON

-

CHARLOTTE

-

BUCHAREST

NEW YORK

BOSTON

HOUSTON

MONTREAL

LONDON

CHARLOTTE

BUCHAREST

What We Do

-

Develop and Implement

We develop and implement quantitative models, risk management and trading systems, and other quantitative analysis tools.

-

Provide Innovative Solutions

We leverage the latest advances in technology, machine learning, and data science to help our clients manage risk and make better investment decisions.

Discover Our Services

We provide a wide range of services that can help meet the needs of our clients. Whether the need is standardized or bespoke we have solutions or resources to help.

Case Studies

Take some time to discover our work and see for yourself the passion and expertise we bring to every project.